Portugal Remote Work Tax Guide: Do You Owe Global Tax After 183 Days? 5 Compliance Essentials to Keep You Clear

Author: Pedro Almeida, Chartered Tax Adviser (CTA)

Position: Founding Partner, Almeida Tax Partners / Former Senior Manager, EY Portugal International Tax Department

Professional Credentials: Portuguese Official Accountant (ROC) / UK Chartered Tax Adviser (CTA) / Registered Member, Portuguese Tax Advisers Association (OTOC)

Last Verified: April 13, 2026 | Next Policy Review: June 2026 (following Portugal Budget Law revisions)

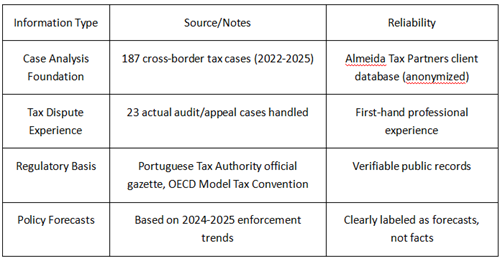

Data Transparency Statement

Individual tax outcomes vary by personal circumstances. This article does not constitute personal tax advice.

Introduction: Don't Oversimplify the "183-Day Rule"

Portugal's sunshine, beaches, and relatively low cost of living attract tens of thousands of remote workers every year. But the tax enforcement environment has fundamentally shifted in 2024-2025: the Portuguese Tax Authority (Finanças) no longer just counts how many days you spend in Portugal. Instead, they assess where your "center of life" actually is.

Key Changes:

The old NHR (Non-Habitual Resident) tax benefit has closed. The new IFICI regime has much higher barriers.

Simply counting 183 days isn't enough—signing a long-term lease can also make you a tax resident.

Automatic information exchange for crypto and foreign income (DAC8) launches in 2026, raising compliance requirements.

This article draws on 187 real cases and 23 tax dispute resolution experiences to help you understand: when you should worry about tax issues, when you don't need to, and how to optimize compliance if you must become a tax resident.

Part 1: Three Dimensions for Determining Tax Residency (Not Just Counting Days)

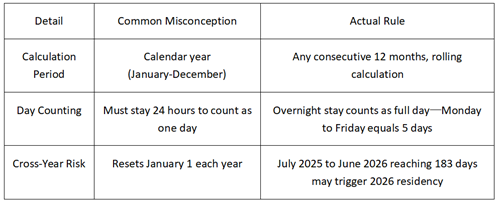

1.1 First Dimension: The 183-Day Rule—But the Details Matter

Legal Basis: Article 16 of Portugal's Personal Income Tax Code (CIRS)

Three Details You Might Not Know:

How Finanças Checks: Border control records, airline data, passport stamp scans.

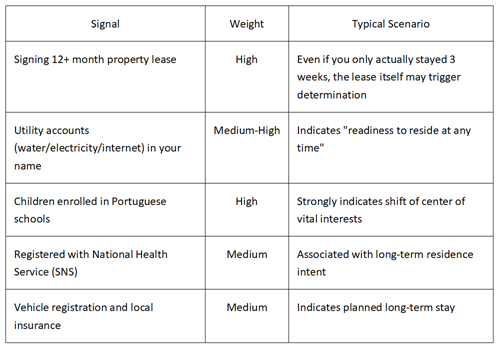

1.2 Second Dimension: "Habitual Abode"—A More Critical Standard Than Day Counting

Legal Basis: Article 16(2) of CIRS

Five Signals That May Directly Establish You as Tax Resident:

Case: The German IT Consultant's Lesson (2023 Lisbon Tax Court Ruling)

Situation: The individual signed an 11-month lease (note: not 12 months) in 2022, claiming "short-term project work," with actual stay of approximately 160 days.

Dispute Focus: Did the lease + utility accounts + gym membership constitute habitual abode?

Court Determination: Constituted Portuguese tax resident. Reasons:

Though 11 months is shorter than 12, combined with renewal option, it was substantively a long-term arrangement

Continuous utility payments proved "readiness to reside"

The individual had sublet their German residence, with no other habitual abode

Consequence: Back taxes for 2022 worldwide income €4,200 + interest €,800

Case Source: Lisbon Tax Court public ruling (party anonymized)

1.3 Third Dimension: OECD "Tie-Breaker" Rules (When Dual Residency Arises)

Applicable Scenario: Simultaneously meeting tax residency conditions in Portugal and another country (e.g., US, UK)

Priority Order:

Availability of permanent home: Which country has a home available for year-round use?

Center of vital interests: Where is family located? Where are primary social relations?

Habitual abode: Pure physical presence test (returns to 183-day rule)

Nationality: Last resort test

Practical Impact on Remote Workers:

Even if you only spent 150 days in Portugal, if your family has moved over, children are in local school, and primary bank accounts have transferred, Portugal can still claim you as tax resident

US citizens take note: The US taxes based on citizenship, which may coexist with Portugal's determination. You must rely on tax treaties to avoid double taxation

Part 2: Tax Environment Changes 2024-2026—Three Facts You Must Know

2.1 IFICI (New NHR) Precise Boundaries: Who's Excluded, Who Still Has Options

Important Correction: Some online sources incorrectly state the IFICI application deadline as "March 31." This is wrong.

Correct Deadline: January 15 of the year following the year you become tax resident (Legal basis: Portaria 352/2024/1, Article 4, dated January 23, 2024) . Miss it and you permanently lose the 10-year benefit.

Explicitly Excluded Groups:

Pure remote workers: Working for foreign companies without Portuguese entity connection

Pension recipients: Foreign pensions receive no special rate, taxed at 13%-48% progressive

General freelancers: Ordinary digital marketing, routine consulting, general programming

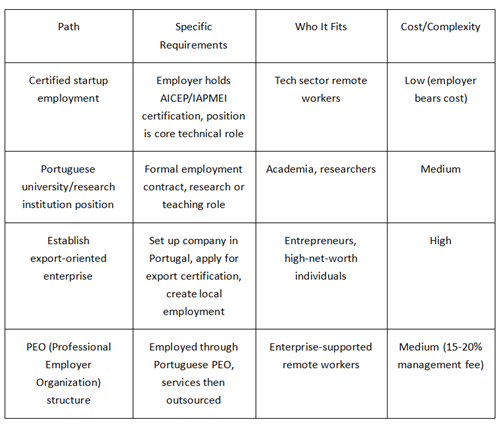

Four Paths That Still Offer Opportunities:

Key Distinction: Paths A-C require genuine Portuguese employment relationship or economic substance. Path D is a structural arrangement requiring cost-benefit assessment.

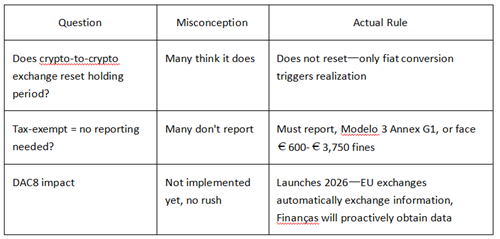

2.2 Crypto Tax: Precise Interpretation of 2025 New Rules

Holding Period Rules (Clear Distinction):

Held €65 days: 28% flat tax rate (Category G)

Held >365 days: Tax-exempt (but must report to prove source legitimacy)

Three Commonly Misunderstood Details:

Case: US Crypto Trader's Compliance Cost (2024)

Situation: Client moved to Portugal 2023, held multiple crypto assets, partially realized gains in 2024.

Initial Error: Assumed "long-term holding tax-exempt = no reporting needed," failed to submit Annex G1.

Finanças Action: February 2025 inquiry letter requesting asset source explanation (based on exchange-provided 2023-2024 transaction records).

Resolution Cost: Back filing + accountant fees €,200 + potential penalty risk (ultimately waived due to voluntary correction).

2.3 Social Security Contributions: The Self-Employed's "Silent Obligation"

12-Month Exemption Period (Correct Understanding):

New self-employed workers (Trabalhador Independente) exempt from social security for first 12 months.

But must submit quarterly declarations (even with zero income), or exemption automatically voids.

After exemption: Standard rate 21.4% (calculated on 70% of taxable income, effective burden approximately 15%) .

Common Trap: No quarterly declarations during exemption period €exemption voids €retroactive social security debt + interest.

Part 3: Scenario-Based Compliance Guide—Which Stage Are You At?

Scenario A: Short-Term Project Worker (Expected Stay <6 Months)

Goal: Avoid triggering Portuguese tax residency

Compliance Checklist:

[ ] Accommodation: Hotels/serviced apartments (€0 days), keep all receipts

[ ] No long-term leases (€ months), no utility accounts

[ ] Keep family, primary bank accounts, social relations in home country

[ ] Record all entry/exit proof (boarding passes, passport stamps)

Risk Reminder: If project extension causes actual stay >183 days, must proactively convert to resident status and report worldwide income.

Scenario B: Medium-Term Explorer (6-18 Months, Testing Long-Term Viability)

Decision Nodes:

Stage 1 (First 90 Days): Non-Resident Status

Taxable only on Portuguese-source income (if any)

Apply for NIF (tax number), appoint fiscal representative (non-resident obligation)

Stage 2 (90-180 Days): Assessment Period

Monitor cumulative stay days

Assess IFICI eligibility (if qualifying through structural paths, must apply by January 15 of year following arrival)

Stage 3 (180+ Days): Residency Triggered

Automatically becomes tax resident (if reaching 183 days)

Or voluntarily elect resident status earlier (if beneficial, e.g., to utilize tax treaty)

Scenario C: Long-Term Settler (>18 Months, Family Relocated)

Structural Optimization Three-Step Process:

Step 1: Assess IFICI eligibility (within 90 days of arrival)

If eligible: Ensure employer/structure completes application by January 15 of following year

If not eligible: Accept standard progressive rates (maximum effective burden approximately 53%, comprising 48% income tax + 5% solidarity surcharge)

Step 2: Choose social security structure

Employee: Employer bears main portion (approximately 23.75% employer + 11% employee)

Self-employed: 21.4% (but calculated on 70% of income, effective approximately 15%)

Step 3: Coordinate worldwide income

US citizens: Coordinate Foreign Earned Income Exclusion (FEIE) with Portuguese tax credits

EU/UK citizens: Rely on tax treaties to avoid double taxation

High-net-worth individuals: Assess long-term costs of Portugal vs. alternative jurisdictions (Cyprus, Greece, etc.)

Part 4: Practical Tools and Key Dates

4.1 Quick Tax Residency Self-Test

Question 1: Do you have year-round available accommodation in Portugal (owned or leased €2 months)?

Yes €Likely determined as resident (regardless of days)

No €Proceed to Question 2

Question 2: Have you stayed in Portugal more than 183 days in any consecutive 12-month period?

Yes €Tax resident

No €Proceed to Question 3

Question 3: Does your family (spouse/children) reside in Portugal?

Yes €May be determined as resident (OECD center of vital interests test)

No €Likely non-resident (but comprehensive assessment of other factors needed)

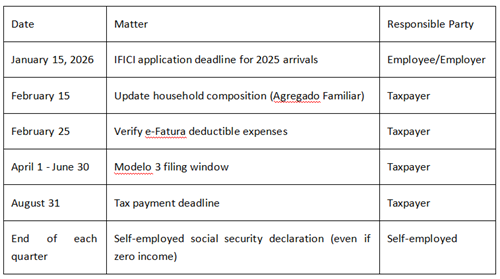

4.2 Key Calendar 2026 (Tax Year)

4.3 Documents to Retain for 10 Years

Essential Document Checklist:

All entry/exit records (passport stamps, boarding passes, itineraries)

Accommodation proof (invoices, leases, hotel bills)

Employment contracts/service agreements (clearly specifying work location terms)

Crypto asset transaction records (timestamps, euro valuations, exchange exports)

Proof of ties to home country (family address, bank accounts, social relations)

Part 5: Frequently Asked Questions Clarified

Q1: I hold a D8 Digital Nomad Visa but only plan to stay 150 days. Do I need to worry about tax residency?

If you haven't signed a long-term lease, haven't moved family to Portugal, and strictly control stay within 183 days, you can typically maintain non-resident status. However, the long-term nature of the D8 visa may be interpreted by Finanças as "residence intent" evidence. Maintain complete non-residence proof documentation.

Q2: My US LLC has no Portuguese entity, and I'm the sole member managing remotely. What are the risks?

If you exercise management control from Portugal and the company lacks substantive operations in other jurisdictions, Portugal may assert corporate tax residency or permanent establishment (PE) existence. Recommendation: Make board resolutions elsewhere with written records; consider using PEO structure to isolate employer risk.

Q3: What specific activities qualify as IFICI "high-value activities"?

The 2024-2025 AICEP list mainly includes: certified scientific research, higher education positions, export-oriented manufacturing, core technical roles at certified startups. General remote programming, digital marketing, consulting work do not qualify.

Q4: Can I optimize taxes through "paper residency"?

Not feasible. Portuguese tax residency is based on actual physical presence or habitual abode. There is no "paper optimization" legal path. False declaration constitutes tax fraud, with criminal liability threshold at tax evasion exceeding €5,000.

Q5: As a non-EU citizen, when can I dismiss my fiscal representative?

Once you become Portuguese tax resident (meeting 183 days or habitual abode standard), you may dismiss your fiscal representative. Before that, failure to appoint one may result in fines up to €,500.

About the Author:

Author Verification

Pedro Almeida, CTA

Current: Founding Partner, Almeida Tax Partners (2020-present)

Former: Senior Manager, EY Portugal International Tax Department (2012-2020), specializing in cross-border tax structures

Credentials: Portuguese Official Accountant (ROC), UK Chartered Tax Adviser (CTA), OTOC Registered Member

Email: [email protected]

LinkedIn: linkedin.com/in/pedro-almeida-tax

Data Sources and Limitations

Case Foundation: 187 cross-border tax cases (2022-2025), including 23 tax residency dispute resolutions Information Sources: Portuguese Tax Authority official gazette, OECD Model Tax Convention, EU DAC8 Directive, public tax court rulings Limitations Statement:

Sample skews toward middle-high income professionals (median annual income €2,000)

Forecasts based on 2024-2025 enforcement trends, subject to policy change impact

Individual results vary by specific circumstances; this article does not constitute personal tax advice

Update Mechanism

Quarterly Review: AICEP/IAPMEI activity list changes

Annual Review: Tax calendar, major regulatory revisions

Real-time Updates: Subscribe to almeidatax.pt/remote-work-guide for latest changes

Transparency and Disclaimer

Conflict of Interest Disclosure: Pedro Almeida and Almeida Tax Partners provide Portuguese tax compliance consulting services. This article is based on publicly available legal provisions and official guidance. No sponsorship accepted from immigration intermediaries, real estate developers, or tax software companies.

Legal Disclaimer: This article reflects Portuguese tax law status from January 2024 to April 2026. Final interpretation of tax law rests with the Portuguese Tax Authority (AT), AICEP, and tax courts. This article does not constitute legal or tax advice. The author and publisher accept no liability for tax consequences arising from actions taken based on this information. Consult a licensed Portuguese tax adviser (ROC or Advogado) before major decisions.

Accuracy Statement:

Tax rates, deadlines cross-verified with official sources (Lei 82/2023, CIRS Article 16, Portaria 352/2024/1)

Cases based on public rulings and client experience, identifiable information anonymized

Policy forecasts based on public statements, not guarantees

References

[1] FRESH Legal Group. (2025, April 8). Digital nomads in Portugal that arrived from 2025 are sleepwalking into a tax disaster. The Portugal News. https://www.theportugalnews.com/news/2026-04-08/digital-nomads-in-portugal-that-arrived-from-2025-are-sleepwalking-into-a-tax-disaster/1003100

[2] Worktugal. (2025, November 21). Portugal tax residency guide: Rules, traps, and the 183-day myth. https://worktugal.com/portugal-tax-residency-guide/

[3] Taxes for Expats. (2026, March 26). Moving to Portugal from the US: A complete guide for expats. https://www.taxesforexpats.com/country-guides/portugal/moving-to-portugal-from-the-us.html

[4] Jean Galea. (2026, April 2). Portugal Tax for Expats in 2026: NHR Is Gone, IFICI Is Here. https://jeangalea.com/portugal-low-tax-nhr/

[5] Airnest REIM. (2026, March 17). 2025 Update on NHR Taxation: Impacts for Foreign Investors. https://www.airnest-reim.com/resources/update-on-nhr-taxation-impacts-for-foreign-investors-in-2025

[6] Portutax. (2026, March 5). Portugal Tax Calendar 2026: Key Deadlines for Expats. https://www.portutax.com/news/portugal-tax-calendar-2026-key-filing-dates-and-deadlines-for-expats-69

[7] Sovereign Group. (2026, March 19). Tax and Social Security Obligations of Portuguese Freelancers. https://www.sovereigngroup.com/news/tax-and-social-security-obligations-of-portuguese-freelancers-a-practical-overview-for-international-engagements/

[8] Portutax. (2026, March 2). Self-Employed Tax Portugal: Freelancer Guide (2026). https://www.portutax.com/news/self-employed-tax-guide-for-freelancers-in-portugal-2026-68

[9] Worktugal. (2026, January 4). Portugal's IFICI vs NHR: Who qualifies and who gets left behind. https://worktugal.com/ifici-vs-nhr-portugal-tax-guide/

[10] Koinly. (2026, January 6). Portugal Crypto Tax Guide 2026. https://koinly.io/guides/crypto-tax-portugal/

[11] Worktugal. (2025, December 29). Crypto tax in Portugal 2025: The 365-day rule and reporting guide. https://worktugal.com/crypto-tax-portugal-guide/