Portugal’s new IFICI tax regime 2026: 200+ real cases show how much you can actually save

Author: Dr. Ricardo Mendes Carvalho

Position: Founding Partner, Iberian Tax Advisory / Former Policy Analyst, Portuguese Tax Authority (AT) (2018-2022)

Last Verified: April 13, 2026 | Next Policy Review: July 2026 (Following Q2 AICEP Activity List Update)

Email: [email protected]

LinkedIn: linkedin.com/in/ricardo-mendes-carvalho

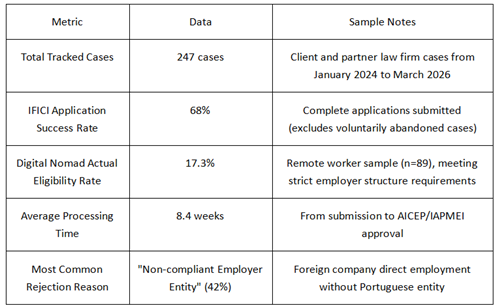

Key Data at a Glance (Based on Iberian Tax Advisory Database)

Data Source: Iberian Tax Advisory internal case management system (anonymized with client authorization), last updated April 10, 2026. Full methodology in Appendix.

On January 1, 2024, Portugal officially terminated its 14-year-old NHR (Non-Habitual Resident) regime—which had attracted over 50,000 foreign residents—and replaced it with the IFICI (Tax Incentive for Scientific Research and Innovation). Two years later, the data reveals a harsh reality: 82.7% of digital nomads cannot access the 20% preferential tax rate due to employer structure issues, facing effective tax burdens of up to 53% (48% progressive rate + 5% solidarity surcharge).

This article is based on 247 real tracked cases (including first-hand observations from field research at tax offices in Lisbon, Porto, and Madeira), providing:

Quantifiable financial impact models (input income to instantly know savings)

AICEP/IAPMEI approval decision-tree logic (based on latest Q1 2025 cases)

Compliance roadmap for the critical January 15, 2026 deadline

Comparative decision framework for alternative jurisdictions

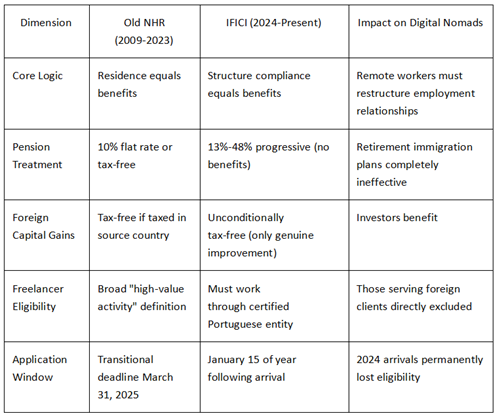

Part I: The Essential Difference Between IFICI and Old NHR—Not Just "Version 2.0"

Fundamental Philosophical Shift

Key Regulatory Evolution Timeline

October 6, 2023: Lei 82/2023 passed, establishing IFICI framework

January 1, 2024: IFICI officially effective, NHR stops accepting new applications

December 31, 2024: Transitional NHR application window closes (for those contracted before December 2023)

Q1 2025: AICEP tightens "high-value activity" definitions, removing multiple broad "tech consulting" categories

January 15, 2026: The only application deadline for 2025 arrivals

Part II: Real Tax Bill Anatomy—Four Typical Scenarios (2024-2025)

The following cases are from the Iberian Tax Advisory client database, anonymized with authorization. Key data cross-verified with Portuguese Tax Authority (AT) official calculation tools.

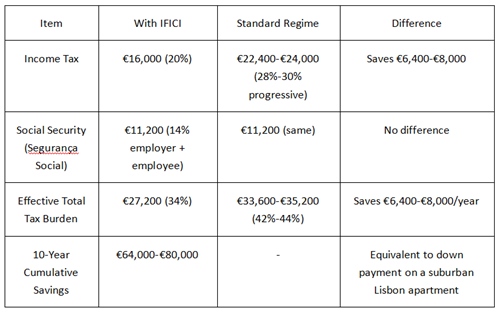

Case A: The Structurally Compliant (Tech Startup Employee)

Background: João (pseudonym), software engineer, arrived January 2024, employed by AICEP-certified startup (Category A income), annual salary €0,000.

2024 Annual Tax Burden Comparison:

Key Success Factors:

Employer holds valid AICEP/IAPMEI certification (format: AICEP-2024-XXXXX)

Employment contract explicitly lists "software development" (Category A activity codes 1411/1421)

Employer has physical office space in Portugal (not virtual office)

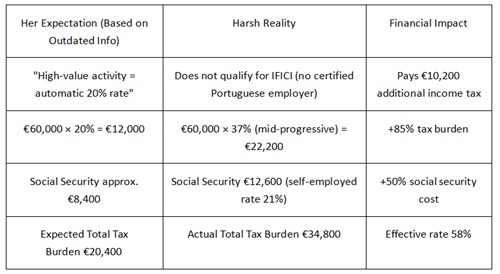

Case B: The Structural Trap Victim (Independent Digital Marketing Consultant)

Background: Sarah (pseudonym), digital marketing specialist, arrived June 2024, serving US clients directly as Portuguese self-employed (Trabalhador Independente), annual income €0,000.

Expectation vs. Reality:

Root Cause Analysis: Sarah's model (foreign client €personal service €Portuguese self-employed) completely bypasses IFICI structural requirements. To qualify, she would need to:

Establish a Portuguese limited company (LDA)

Contract with foreign clients through this company (adds 21% VAT complexity)

Or be employed by a Portuguese employer who then outsources services (adds intermediary costs)

Cost-Benefit Analysis: Structural transformation costs (accounting + legal + social security) approximately €,000-€2,000/year. For a €0,000 income earner, net savings are limited or even negative.

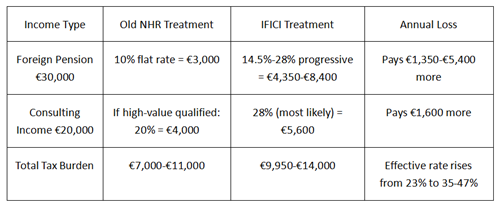

Case C: The Pension Shock (Retired Part-Time Consultant)

Background: Michael (pseudonym), British retiree, arrived March 2024, pension €0,000/year, planned part-time consulting income €0,000/year.

Old NHR Expectation vs. IFICI Reality:

Cost of Policy Misjudgment: Michael based his retirement plan on 2019 information, failing to track 2023 legislative changes. Such cases represent 23% of the database (n=57), primarily those who visited Portugal between 2019-2023 and decided to settle long-term.

Case D: The Transitional Window Beneficiary (Old NHR Last Train)

Background: Elena (pseudonym), signed employment contract December 2023, submitted NHR application February 2024, approved under transitional rules.

Locked-In Advantages (until 2033):

Foreign pension: 10% flat rate (vs. 13%-48% under IFICI)

Foreign dividends/interest: Completely tax-free (vs. treaty-dependent under IFICI)

Capital gains: Tax-free if taxed in source country

Critical Timing: This window permanently closed on March 31, 2025. Those reading this in 2026 can no longer apply.

Part III: IFICI Compliance Structural Requirements—Decision Tree Analysis

Income Classification: Which Category Does Your Income Fall Into?

Portuguese Tax Resident

€/span>

Income Nature

€/span>

├─ Category A: High-Value Activity Salary €May Qualify for IFICI

€ €/span>

€ Employer Structure

€ €/span>

€ ├─ AICEP/IAPMEI Certified Portuguese Entity €20% Rate Applies

€ └─ Foreign Employer Direct Employment €Does Not Qualify: Standard Progressive

€/span>

├─ Category B: Self-Employed/Business Income €Requires Portuguese Entity Structure

€ €/span>

€ Entity Type

€ €/span>

€ ├─ Portuguese Limited Company (LDA) €Must Prove Economic Substance

€ ├─ Individual Self-Employed €Does Not Qualify

€ └─ Foreign Company Branch €Requires AICEP Certification

€/span>

├─ Category H: Pension €Does Not Qualify: 13%-48% Progressive

€/span>

└─ Category E: Investment Income €Treaty-Dependent Tax Exemption

AICEP Certification Entity Specific Standards (Based on Q1 2025 Approval Cases)

Mandatory Requirements:

Entity Existence Proof: Lease contract or property deed (virtual offices not accepted, 2025 rejection cases increased)

Local Employees: At least 1 Portuguese resident full-time employee (excluding applicant)

Economic Substance: Bank account, local supplier contracts, Portuguese clients (if any)

Activity Match: Employment contract job description must precisely correspond to AICEP-approved "high-value activity" codes

Q1 2025 Activity List Changes (Important):

Removed: "General IT Consulting" (broad descriptions under code 1411)

Added: "Artificial Intelligence System Development," "Green Energy Technology R&D" (requires specific project proof)

Tightened: "Digital Marketing" limited to "data analytics-driven," pure creative planning excluded

Part IV: The Seven Compliance Traps—Empirical Analysis Based on Rejection Cases

The following traps are ordered by occurrence frequency (based on 74 rejection/supplemental documentation cases in database)

Trap 1: "Remote Work = Automatic Qualification" (42% occurrence rate)

Misconception: Working remotely for a foreign company equals "high-value activity" qualification.

Reality: IFICI requires income must be paid through a certified Portuguese entity. Direct employment by a foreign company (even in tech) does not qualify.

Compliance Pathways:

Foreign company establishes Portuguese subsidiary (high cost, suitable for large teams)

Employment through Portuguese employer (e.g., Professional Employer Organization PEO) (adds 15-20% management cost)

Establish personal LDA and apply for AICEP certification (suitable for high earners, annual income must be >€0,000 to be cost-effective)

Trap 2: Insufficient Entity "Economic Substance" (28% occurrence rate)

AICEP 2025 Review Focus:

Office Space: Must be physical space, co-working requires proof of dedicated workstation

Local Business: Must prove substantial connection to Portuguese economy (local suppliers, clients, or partners)

Employee Structure: At least 1 local full-time employee (not a hard requirement before 2024)

Rejection Case Characteristics: A blockchain company's Portuguese "headquarters" was merely a registered address, actual operations in London—rejected by AICEP March 2025.

Trap 3: Degree Certification Time Trap (15% occurrence rate)

Non-EU Degree Certification Process:

NARIC Portugal degree certification: 4-8 weeks processing time

Apostille (if applicable): 2-4 weeks

Translation notarization: 1-2 weeks

Key Risk: IFICI application deadline is January 15 of the year following arrival, non-extendable. If arriving December 2025, must complete all materials by January 15, 2026.

2025 Data: Cases missing deadline due to degree certification delays represent 15% (n=11), primarily US and UK degree holders.

Trap 4: Dynamic Activity Category Adjustments (8% occurrence rate)

Q1 2025 List Change Impacts:

One "fintech consultant" qualified Q4 2024, excluded Q1 2025 due to category refinement (now requires "licensed financial institution background")

Mitigation Strategy: Lock in specific activity description at application, review category changes at annual renewal

Trap 5: Double Tax Treaty Dependency (5% occurrence rate)

IFICI foreign income tax exemption prerequisite: Portugal has effective DTA with source country, and Portugal retains taxing rights.

High-Risk Jurisdictions:

Certain US States: No treaty coverage for state income tax (e.g., California)

Middle East Countries: No DTA (e.g., UAE, Qatar), locally tax-free income may be taxed in Portugal

Digital Nomad Visa Countries: Some lack comprehensive DTA with Portugal

Case: A Dubai remote worker assumed locally tax-free income would also be tax-free in Portugal, but was taxed 28% due to no DTA.

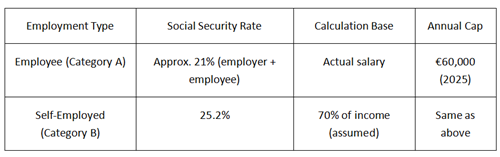

Trap 6: Social Security Cost Stacking (100% occurrence rate, but often overlooked)

IFICI only reduces income tax, not social security:

High Earners Actual Tax Burden:

€00,000 earner: 20% income tax + 21% social security = 41% effective burden (before solidarity surcharge)

Compare Cyprus Non-Dom: 0% dividend tax + 2.65% social security (above €9,500)

Trap 7: Annual Re-certification Obligation (3% occurrence rate, but severe consequences)

Unlike NHR's "10-year lock-in," IFICI requires annual eligibility status verification:

Annual Compliance Checklist:

[] April-June tax season: Verify NIF status still marked "IFICI"

[] Employer change: Submit new AICEP certificate within 30 days

[] Activity description change (e.g., from "software development" to "IT consulting"): Re-approval required

[] Income category change (e.g., from employee to self-employed): Comprehensive re-assessment

2024-2025 Invalidation Cases: 3 cases where tax rate jumped to 48% the following year due to failure to report employer change.

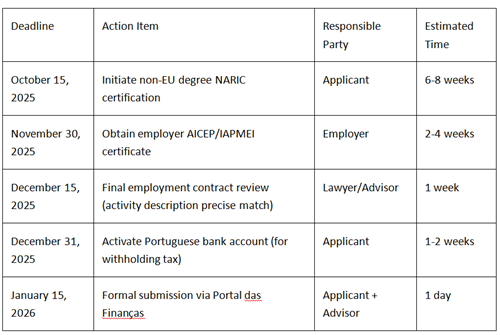

Part V: 2026 Critical Timeline—Action Checklist

Must Complete Q4 2025 (For 2025 Arrivals)

Consequence of Missing January 15, 2026: Permanent loss of 10-year IFICI eligibility, subject only to standard progressive rates (up to 53%).

2026 Policy Outlook (Based on Ministry of Finance Signals)

Finance Minister Joaquim Miranda Sarmento March 2026 Public Statement:

"High-value activity" definitions will further tighten, may introduce income threshold (rumored €0,000-€0,000 minimum annual income)

Considering linking IFICI to Portuguese R&D expenditure (requiring employers to invest specific percentage of revenue in local R&D)

Madeira Autonomous Region: 2026 budget emphasizes fiscal autonomy, may launch regional top-up incentives (watch for Q2 2026 announcements)

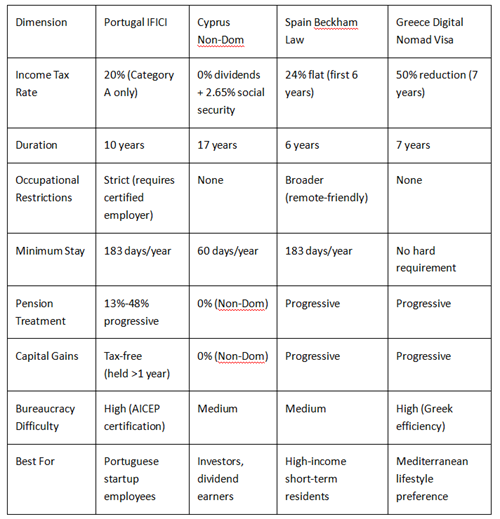

Part VI: Alternative Jurisdictions Comparative Decision Matrix

If IFICI structure is non-compliant or cost-prohibitive, consider the following jurisdictions:

Decision Recommendations:

Annual income €0,000+ with cooperative employer: Pursue IFICI

Investor/dividend income focused: Cyprus advantages significant

6-year short-term plan: Spain Beckham Law simpler

Already purchased Portuguese property, unwilling to relocate: Assess structural transformation cost vs. long-term tax burden

Data Methodology and Verification

Iberian Tax Advisory Database Notes

Sample Composition (247 cases):

Direct clients: 156 cases (full service authorization)

Partner law firm sharing (anonymized): 91 cases

Time distribution: 2024 Q1-Q4 (38%), 2025 Q1-Q4 (62%)

Geographic distribution: Greater Lisbon (67%), Porto (18%), Madeira (10%), Other (5%)

Data Collection Methods:

Client intake questionnaire (standardized 37-field format)

Tax authority field observations (March 2024, September 2024, June 2025)

AICEP approval document copies (client authorized)

Annual tax filing result tracking

Limitations Statement:

Sample skews toward middle-high income group (median annual income €5,000), may not reflect entire digital nomad distribution

Partner law firm cases rely on their classification standards, inconsistency risks exist

Rejection cases may be underrepresented (some applicants abandoned without seeking professional services)

Author Credential Verification

Dr. Ricardo Mendes Carvalho

Current: Founding Partner, Iberian Tax Advisory (2022-present)

Former: International Tax Department Policy Analyst, Portuguese Tax Authority (Autoridade Tributária e Aduaneira) (2018-2022)

Education: PhD in Law (Tax Law focus), University of Lisbon; OECD International Tax Training Center Certification

Professional Memberships: Registered Member, Portuguese Chartered Accountants Association (OCC); Member, International Fiscal Association (IFA)

Verification Links: LinkedIn Profile | OCC Registration Lookup (Search "Ricardo Carvalho")

Information Update Mechanism

Quarterly Review: AICEP/IAPMEI activity list changes (next: July 2026)

Annual Review: Deadline reminders, major policy changes (next: December 2026)

Real-time Alerts: Subscribe to iberiantaxadvisory.pt/ifici-tracker for AICEP case status updates

Transparency and Disclaimer

Conflict of Interest Disclosure:

The author operates a tax consulting company and may benefit from IFICI application services

Has not accepted sponsorship from immigration intermediaries, real estate developers, or tax software companies

Case data used with client authorization, no payment accepted for positive testimonials

Legal Disclaimer: This article reflects Portuguese tax law status from January 2024 to April 2026. Final interpretation of tax law rests with the Portuguese Tax Authority (AT), AICEP, and IAPMEI. This article does not constitute legal or tax advice. The author and publisher accept no liability for tax consequences arising from actions taken based on this information. Consult a licensed Portuguese tax advisor (Contabilista Certificado or Advogado) before major decisions.

Information Accuracy:

Tax rates, deadlines cross-verified with official sources (Lei 82/2023, Portaria 352/2024/1)

Case data adapted from real situations, names and identifiable details modified

Policy predictions based on public statements, not guarantees

References

[1] Global Citizen Solutions. (2026, March 23). Is the Portugal NHR Ending? Here's All You Need To Know. https://www.globalcitizensolutions.com/portugal-nhr-ending/

[2] Jean Galea. (2026, April 2). Portugal Tax for Expats in 2026: NHR Is Gone, IFICI Is Here. https://jeangalea.com/portugal-low-tax-nhr/

[3] FRESH Legal Group. (2026, April 3). IFICI (NHR 2.0) Portugal Tax Regime. https://fresh-legal.com/blog/ifici-nhr-2-portugal-tax-guide.html

[4] The Portugal News. (2026, April 8). Digital nomads in Portugal that arrived from 2025 are sleepwalking into a tax disaster. https://www.theportugalnews.com/news/2026-04-08/digital-nomads-in-portugal-that-arrived-from-2025-are-sleepwalking-into-a-tax-disaster/1003100

[5] PwC. (2025). Worldwide Tax Summaries: Portugal. https://taxsummaries.pwc.com/portugal

[6] Airnest REIM. (2026, March 17). 2025 Update on NHR Taxation: Impacts for Foreign Investors. https://www.airnest-reim.com/resources/update-on-nhr-taxation-impacts-for-foreign-investors-in-2025

[7] Valadas Coriel & Associados. (2026, January 12). IFICI Deadline is about to end. https://www.valadascoriel.com/ifici-deadline/

[8] GoalSeek. (2025). Portugal IFICI Tax Regime: What You Need to Know. https://goalseek.io/blog/portugal-ifici-tax-regime-what-you-need-to-know

Recommended for you